For California residents, living trusts are a common estate planning tool. Due to high property values throughout the state, especially the San Francisco Bay Area, estate assets can easily reach millions of dollars. Trusts allow asset distributions to beneficiaries without going through the California probate process, avoiding additional costs and saving time when closing an estate.

For California residents, living trusts are a common estate planning tool. Due to high property values throughout the state, especially the San Francisco Bay Area, estate assets can easily reach millions of dollars. Trusts allow asset distributions to beneficiaries without going through the California probate process, avoiding additional costs and saving time when closing an estate.

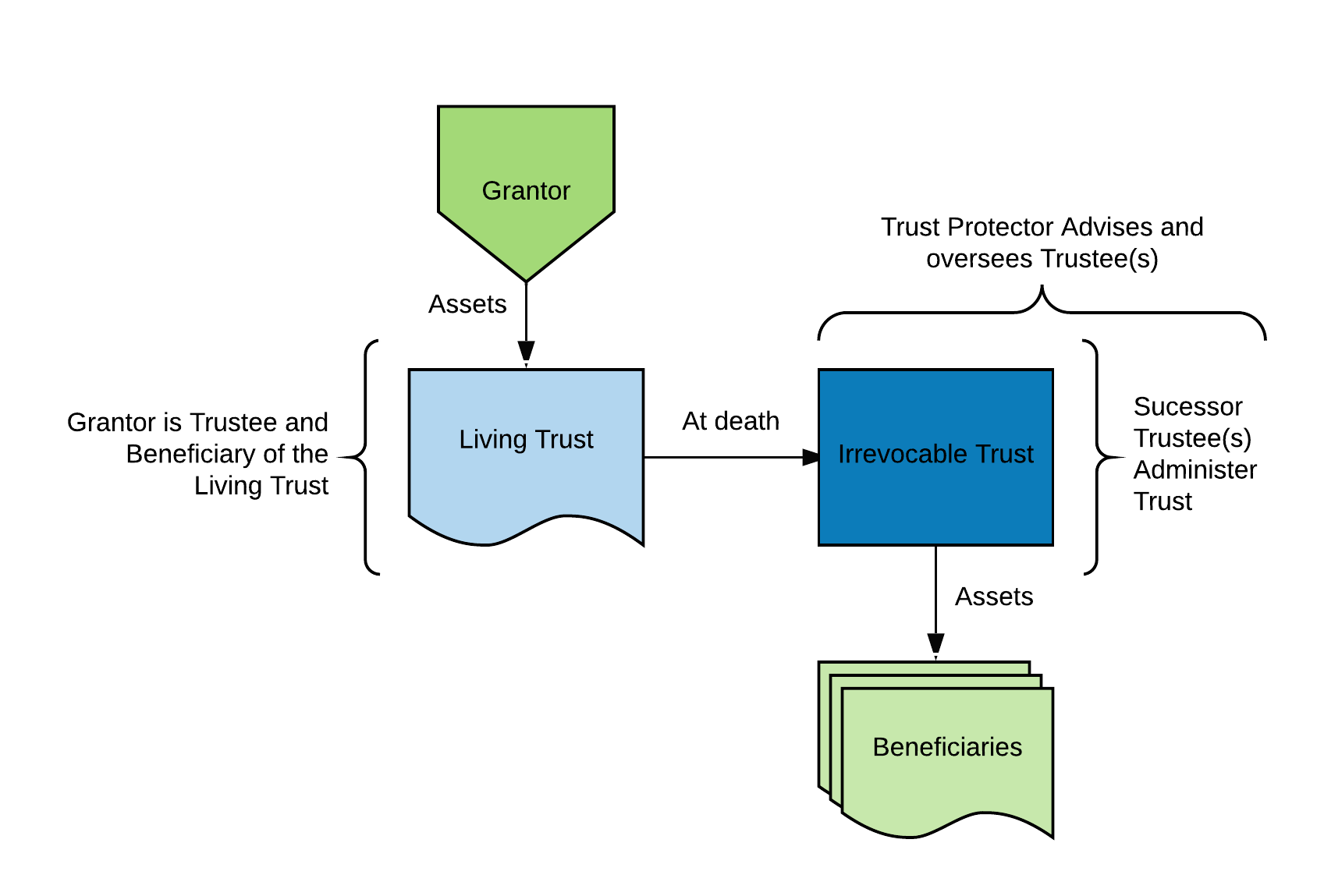

Why Set Up a Living Trust?

In a living trust, as the person creating the trust (the grantor), you place your assets into a revocable trust. While you are alive, you are also the trustee and the beneficiary, and you control your assets. Because the trust is revocable, you can add or sell assets, change beneficiaries, etc. Upon your death, the trust becomes an irrevocable trust. The person(s) you named as your successor trustee(s) then assumes control and administers the assets for the beneficiaries according to your instructions.

The trustee(s) have a fiduciary duty to the beneficiaries. They must put the beneficiaries’ interests before their own at all times while following the mandates in the trust agreement. Many long-term or complicated trusts also name a trust protector, who advises, oversees, and can replace a trustee if necessary. This offers an additional layer of protection for the beneficiaries. Read the rest of this entry »