This year, most people have been stressed (in time, and also cognitively and emotionally as well) more than ever before at home and work. After our busiest spring on record helping clients, we recently brainstormed the best techniques we use internally for staying on track professionally right now: Read the rest of this entry »

Estate Planning, Trusts, & Probate in California

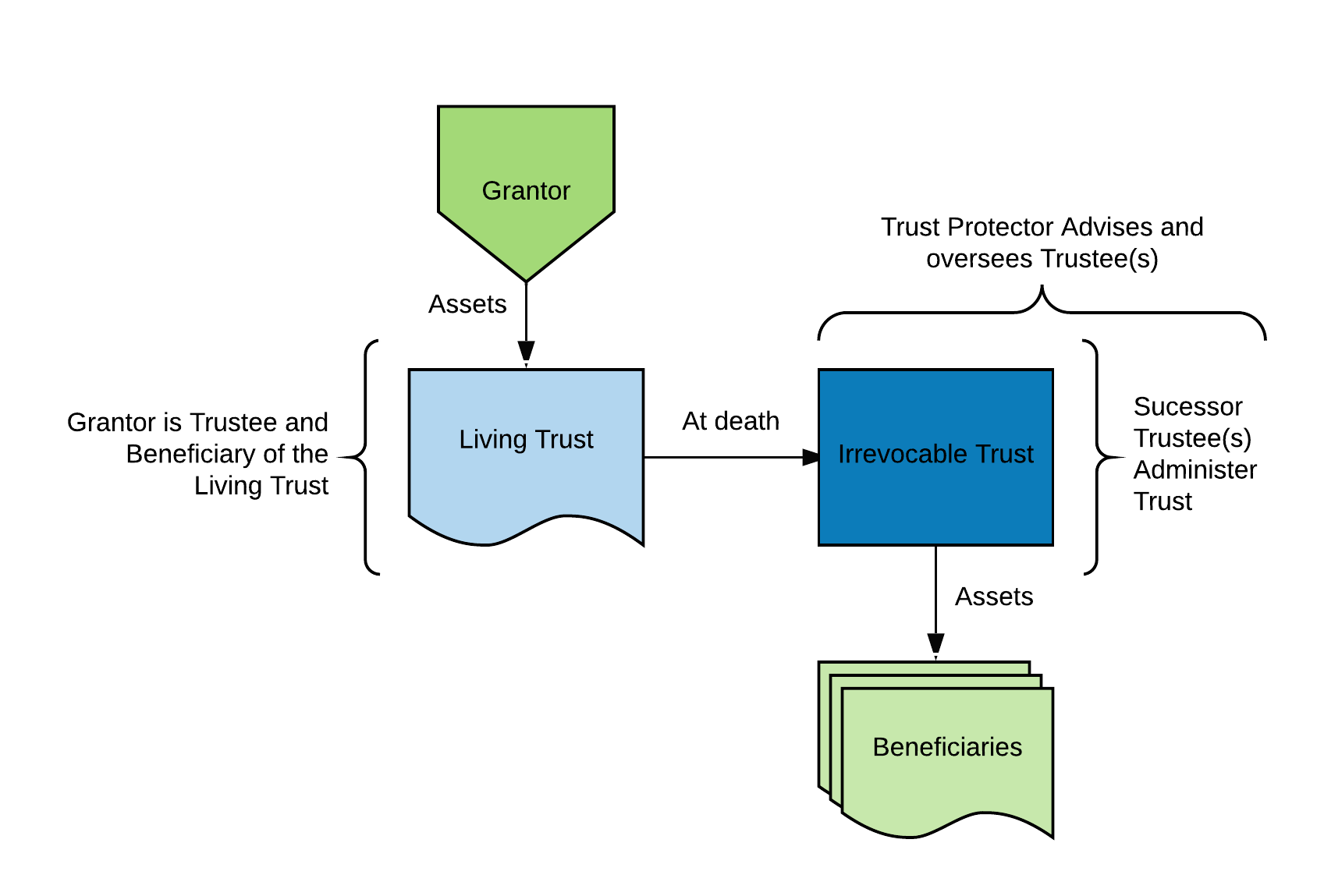

For California residents, living trusts are a common estate planning tool. Due to high property values throughout the state, especially the San Francisco Bay Area, estate assets can easily reach millions of dollars. Trusts allow asset distributions to beneficiaries without going through the California probate process, avoiding additional costs and saving time when closing an estate.

For California residents, living trusts are a common estate planning tool. Due to high property values throughout the state, especially the San Francisco Bay Area, estate assets can easily reach millions of dollars. Trusts allow asset distributions to beneficiaries without going through the California probate process, avoiding additional costs and saving time when closing an estate.

Why Set Up a Living Trust?

In a living trust, as the person creating the trust (the grantor), you place your assets into a revocable trust. While you are alive, you are also the trustee and the beneficiary, and you control your assets. Because the trust is revocable, you can add or sell assets, change beneficiaries, etc. Upon your death, the trust becomes an irrevocable trust. The person(s) you named as your successor trustee(s) then assumes control and administers the assets for the beneficiaries according to your instructions.

The trustee(s) have a fiduciary duty to the beneficiaries. They must put the beneficiaries’ interests before their own at all times while following the mandates in the trust agreement. Many long-term or complicated trusts also name a trust protector, who advises, oversees, and can replace a trustee if necessary. This offers an additional layer of protection for the beneficiaries. Read the rest of this entry »

Callahan Financial Planning Opens San Francisco Financial Advisory Office

San Francisco – Callahan Financial Planning, a fee-only independent personal financial planning and investment management firm with offices throughout the Bay Area, has announced its latest expansion with the addition of a financial advisory office in San Francisco, CA.

“We see this as an incredible opportunity to provide our special fee-only advice to not just those in San Francisco, but also those throughout the peninsula in communities like San Mateo, Redwood City, Palo Alto, South San Francisco, Daly City, along with Oakland and Berkeley in the East Bay”, said Callahan Financial Planning’s Vice President of Financial Planning, Reuben Brauer, CFP®.

Callahan Financial Planning Opens Marin County Financial Advisory Practice in San Rafael, CA

San Rafael, CA – Callahan Financial Planning, a fiduciary financial planning and investment advisory company, has announced the opening of an office in San Rafael, CA following the acquisition of certain assets of the financial advisory firm Gary A. Dossick & Associates. The office is now located at 851 Irwin St Ste 201A, San Rafael, CA 94901.

Clients will be served by a team that includes three Certified Financial Planner™ (CFP®) practitioners, a Chartered Financial Analyst (CFA®) charterholder, an IRS Enrolled Agent, and supporting staff.

Callahan Financial Planning has seen significant growth since opening in 2010. The firm now manages $125 million in client assets, and anticipates opening additional locations in San Francisco and Mill Valley in California, and Denver, Colorado following this expansion.

From this San Rafael office, Callahan Financial Planning anticipates serving clients throughout Marin County, including residents of Mill Valley, Fairfax, Larkspur, Marin City, Corte Madera, San Anselmo, Marinwood, Novato, Sausalito, Tiburon, and Lagunitas-Forest Knolls.

Nebraska 4797N – Special Capital Gains Election for Tax-Free Stock Sales

The Nebraska Special Capital Gains/Extraordinary Dividend Election, elected and claimed on Form 4797N, can provide a substantial tax break for employees who acquire company stock over their years of employment. This election allows employees who own stock in their employer, or former employer, to exclude that stock’s capital gains income from their Nebraska taxable income under certain circumstances.

More and more employers are offering stock purchase plans and stock-based compensation to their employees, which can make for an excellent opportunity to avoid state income tax on capital gains from the sale of a stock in Nebraska. Some questions to consider if you (or your company) might benefit from this rare opportunity in Nebraska tax law:

- Does your employer offer an employee stock purchase program?

- Do you receive employee stock grants from your employer?

- Do you own stock in and work for your own company?

- Did you know that Nebraska offers tax breaks for these situations?

How to Find the Best Financial Advisor Recommended for Your Situation

The financial advice field is a bit convoluted, but this guide can help.

Financial Advisor Fees/Costs

First, there’s how you pay for advice. All financial advice has a cost, but sometimes it’s explicit (e.g., you can see it), and sometimes it’s only implicit (e.g., it’s embedded inside a financial product, and what you’re paying is not easily visible).

Most financial advisors today describe themselves as fee-based advisors. Legally, this means they can (and generally do) perform their activities in two ways: they earn a commission on certain product sales, and a fee on certain investments. The title is a bit misleading in this way, but the moniker persists.

We think this creates a conflict of interest: it often causes (even if only subconsciously) the financial advisor to recommend things that pay them the best compensation over what is in the client’s best interest.

Because of this inherent conflict, a special sub-set of financial advisor was born: the fee-only financial advisor. We recommend anyone seeking financial advice only work with a fee-only advisor.

A national organization lists and ensures fee-only compliance for all of its members; it’s called the National Association of Personal Financial Advisors (NAPFA), and it has an online directory of all of its members. So, for example, you can search for a list of all the fee-only financial advisors in Omaha, NE or the San Francisco, CA Bay Area (cities where we have offices).

Understanding Medicare in Retirement

According to AARP, couples age 65 who retired in 2017 were estimated to pay $275,000 for health care over the course of their retirement. This is a 6% increase over 2016’s projections, and over a 70% increase since annual research began in 2002. The majority of retirees will enroll in Medicare to help cover medical costs during retirement. However, there are several things you need to know about how Medicare works, and how to enroll in order to avoid penalties. Read the rest of this entry »